Insurance Core Platforms in the Age of Agentic AI — Part 2

May 09, 2025

Introduction

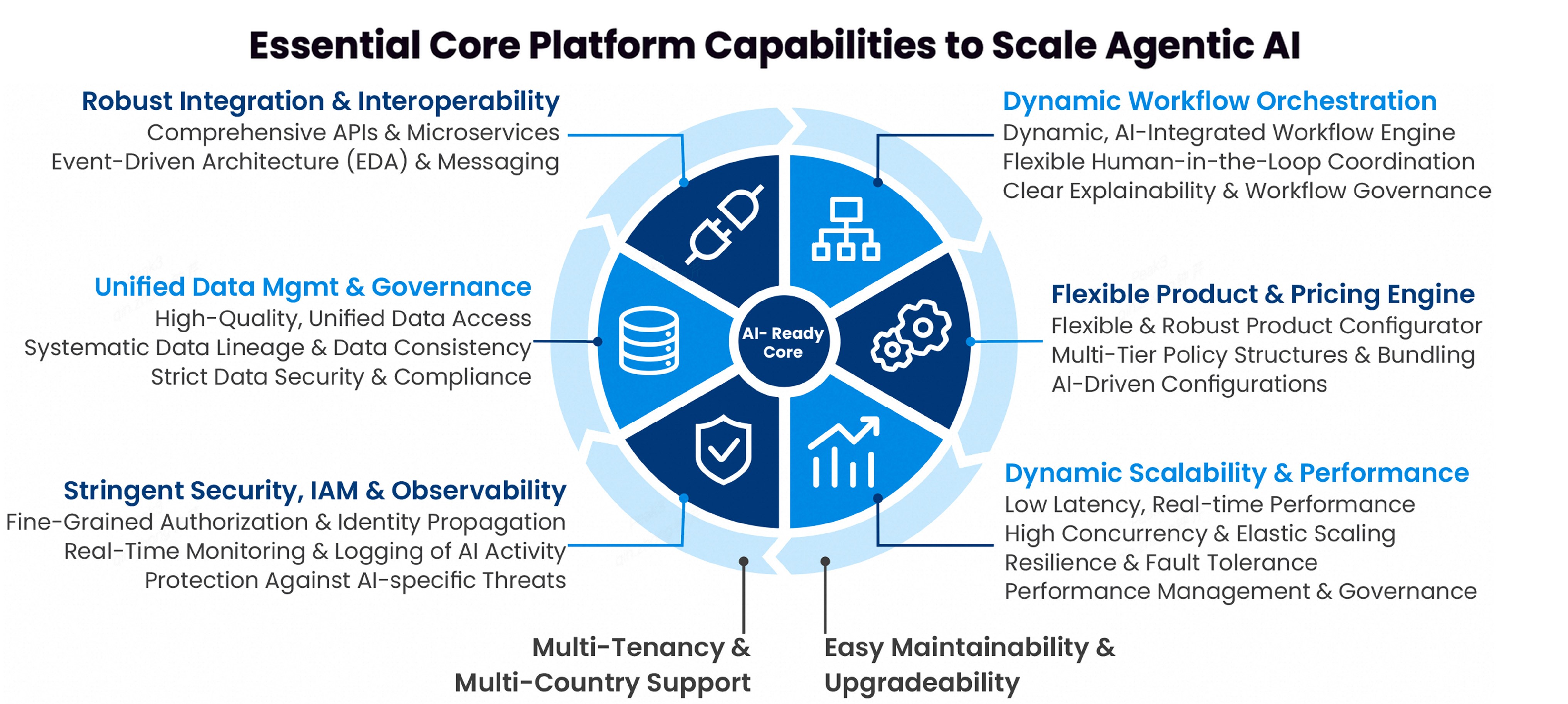

ILLUSTRATION 1 : Essential insurance core platform capabilities to scale Agentic AI

In this Part 2, we discuss key challenges faced by insurers with regards to their core systems and explore different modernization approaches and no-regret moves to meet the requirements set out to successfully scale AI agents. We contrast the benefits and challenges of following a “hollow out the core” approach with a middle-office and addressing core modernization more holistically by adopting an end-to-end, AI-ready core platform.

Do you want to evaluate the AI-readiness of your existing core platform or a new vendor solution, please see this executive checklist for insurance leaders: Is My Core Insurance Platform Ready for Agentic AI? – A Checklist for Insurance CEOs and CIOs

Recommendations

Assess your current systems and potential new vendor solutions against the requirements set out in Part 1 of this paper and your own business requirements to identify key gaps.

Assess the change complexity based on the gap analysis and your internal change capacity to decide on the right modernization approach (i.e., middle-office vs. holistic core modernization).

Keep continued legacy dependencies and duplications in mind when deciding on the right modernization approach.

Systematically evaluate potential solution providers against the requirements set out in Part 1 (and the separate checklist) and rigorously test providers’ marketing promises.

Think in terms of long-term optionality and credible provider roadmaps, putting more emphasis on the future-proof architecture than pure functional requirements.

Accept that no solution meets all requirements fully out-of-the box; be ready to co-innovate together with other insurers and solution providers, adopting a product and not a project mindset.

Prioritize modular solutions that can grow with your needs and avoid throw-away investments into pure middle-office solutions.

Insurers with operations across countries: Strive for solutions supporting multi-tenant and multi-country deployments to multiply benefits by making it easier to build reusable AI agents and train and improve them on larger data sets.

The Current Challenge of Legacy Technology

Choosing the Right Modernization Approach

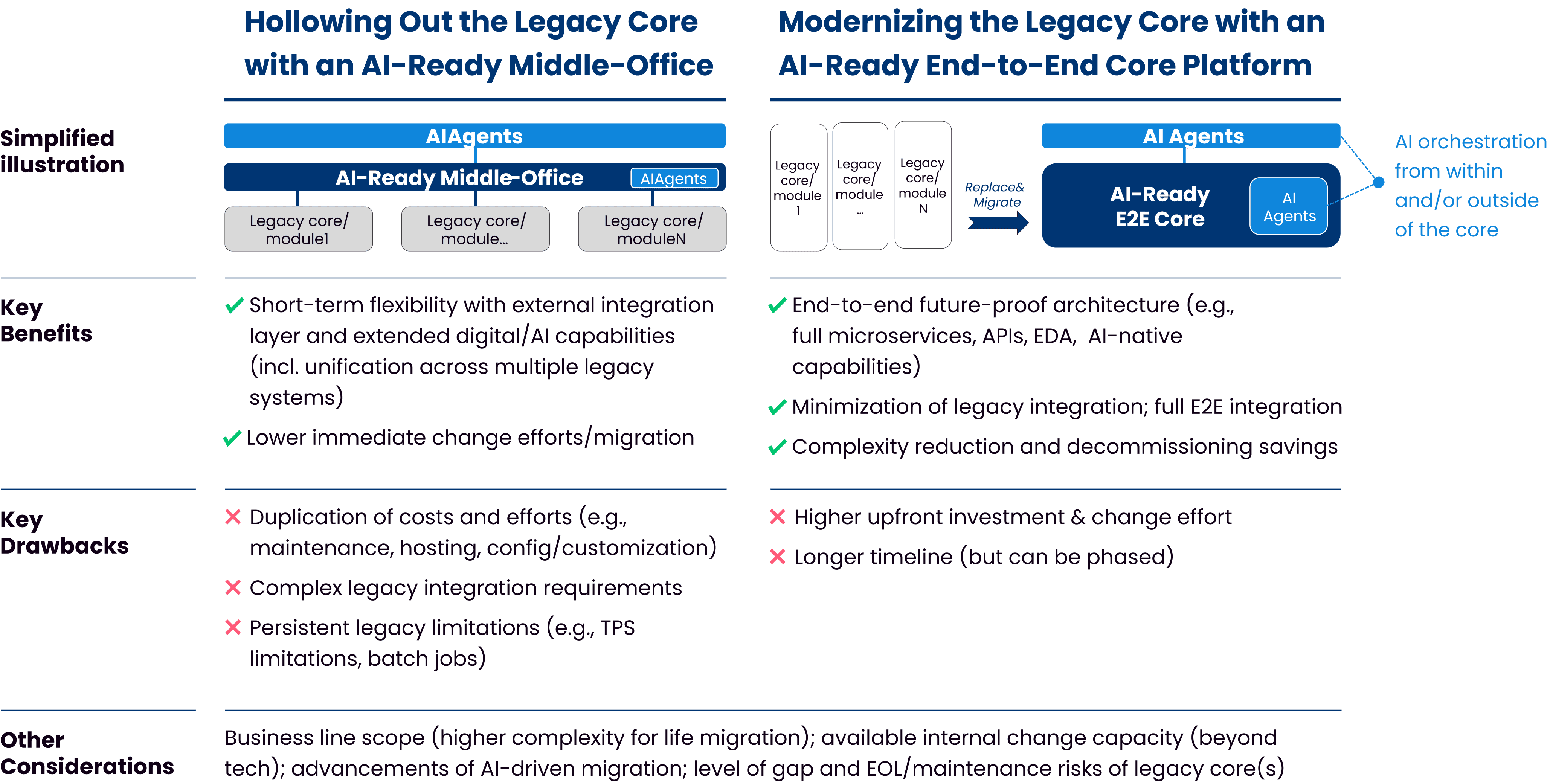

Hollowing Out the Legacy Core with an AI-Ready Middle-Office

Replacing the Legacy Core with an AI-Ready End-to-End Core Platform

Considerations for Choosing the Right Approach

ILLUSTRATION 2 : Comparison of modernization approaches

Build, Buy, or Partner?

Excursion: Regional Modernization and Scalable Agentic AI Strategies

Peak3 and Graphene: Your Enablers for the Agentic Future

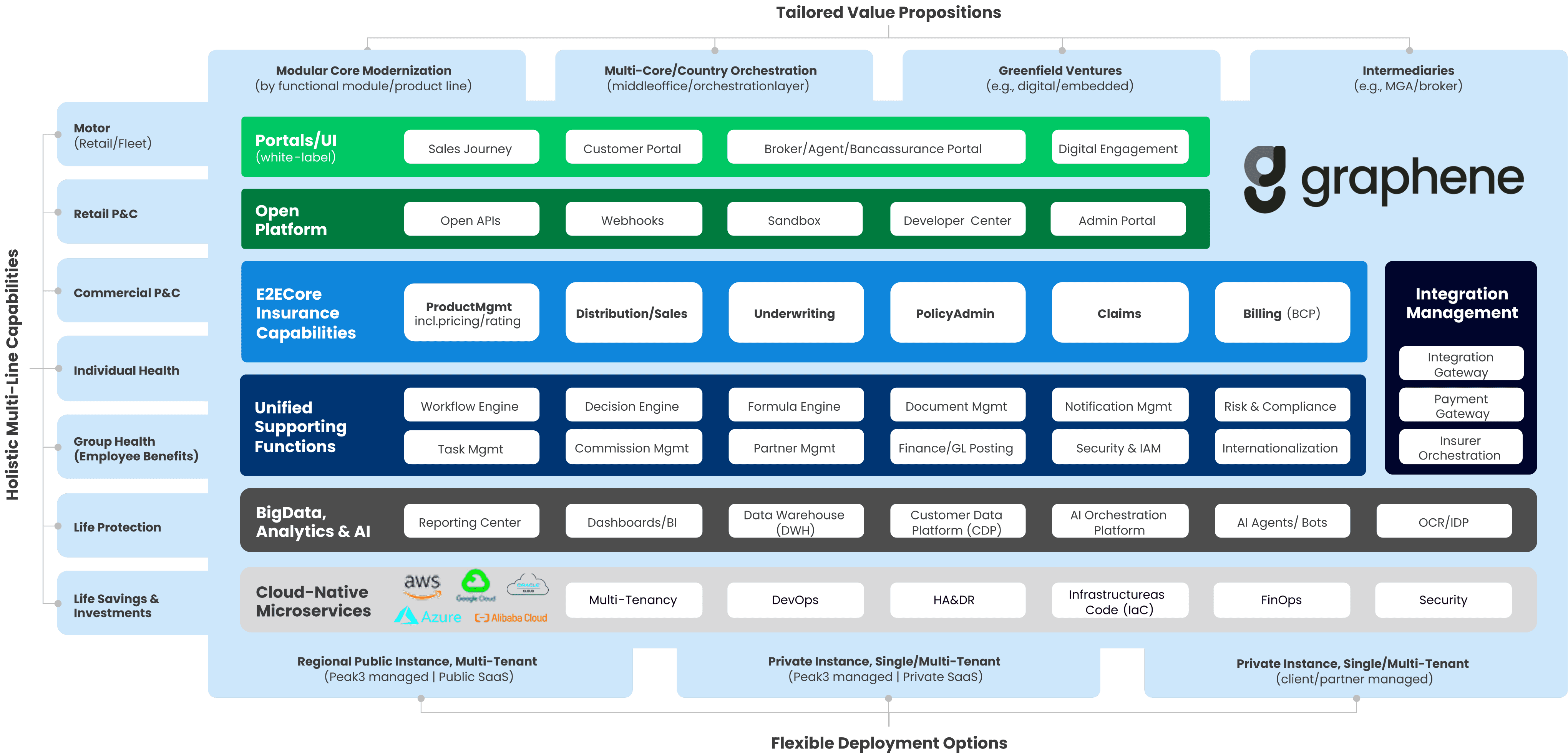

ILLUSTRATION 3: Simplified overview of Graphene by Peak3

Purpose-built from the outset on microservices architecture, Graphene enables flexible modernization strategies and can be deployed flexibly to accommodate your specific circumstances. It can act as a middle-office, replace individual vertical functional modules (e.g., claims), or fully replace and unify your legacy systems horizontally across product lines.

Graphene supports multi-tenant and multi-country deployments. This allows you to build efficient and scalable business models across borders. Graphene is delivered as software-as-a-service (SaaS). This way, you can get started quickly with limited upfront commitment and investments. Furthermore, through regular upgrades, your core stays secure and evergreen.

References

¹ Gartner, Market Guide for Non-Life Insurance Core Platforms, Europe by Sham Gill and James Ingham, 4 March 2025 (for Gartner subscribers only). GARTNER is a registered trademark and service mark of Gartner, Inc. and/or its affiliates in the U.S. and internationally and is used herein with permission. All rights reserved.

² A significant part of value creation can come from the decommissioning of legacy systems. While some parallel operations of legacy and new systems are unavoidable, a core modernization strategy should put similar focus on the decommissioning of the legacy as on the launch of the new platform.

³ Gartner, Market Guide for Life and P&C Insurance Core Systems, APAC by Richard Natale and Sham Gill, 11 February 2025 (for Gartner subscribers only)

________________________________________________________________________

About Peak3

Founded by insurance, digital and technology experts, Peak3 powers the digital operating system of the global insurance industry. We combine insurance core, distribution, and AI solutions to deliver a step change in performance for insurers, MGAs, and insurance intermediaries.

From greenfield embedded insurance ventures to digital-first, multi-country core modernization programs, our cloud-native SaaS solutions power top customers across life, health, and P&C insurance.

Whitepaper

Leveraging AI to automate processes and mitigate fraud

Article

Confidently navigate your core modernization journey